{kind=link}

Snowflake Inc. signage is displayed on a smartphone in an arranged photograph taken in the Brooklyn … [+]

© 2020 Bloomberg Finance LP

Cloud-based data warehousing company Snowflake (NYSE: SNOW) saw its stock decline by almost 30% over the last month. While not much really changed on the ground for Snowflake, which is on track to more than double revenues this fiscal year, there are a couple of factors that have likely driven the sell-off. Firstly, Snowflake stock remains very richly valued trading at over 130x consensus FY’21 Revenues and is up by about 130% from its IPO price. Considering these big gains, investors are likely booking some profits. Secondly, in mid-December Snowflake saw its first lockup release post its IPO, allowing employees to sell 25% of their vested options. While this only had a limited impact, investors are likely concerned that the full lock-up expiration, which happens this March, will put a lot more pressure on the stock. Snowflake’s float, or the shares available to investors for trading, stands at just about 18% of its total shares outstanding currently. Thirdly, with Covid-19 vaccines being rolled out globally, investors could be rethinking their allocation to cloud computing stocks which were a hot theme through the pandemic, while shifting to more value bets. This could also be a factor hurting Snowflake stock.

Our interactive dashboard analysis of Snowflake’s Valuation gives more details on the company’s Revenue, growth, and valuation.

[11/30/2020] Why Snowflake Rallied 20%

Cloud-based data warehousing startup Snowflake (NYSE: SNOW) saw its stock rally by over 20% last week to about $330 per share, valuing the company at about $90 billion. While there wasn’t much news from the company over the past week, there could be a couple of factors that drove up the stock. Firstly, Snowflake is likely to report its first set of quarterly results as a public company on December 2 and investors are likely anticipating strong numbers. For perspective, the consensus estimates that the company will post revenue of about $148 million, and a loss per share of about -$0.26. Separately, investors have continued to double down on high-growth and software stocks through the last week, after taking a breather earlier in the month amid the vaccine news. For example, Zoom gained about 12% over the last week while Tesla

TSLA

Our interactive analysis on Snowflake’s Valuation gives more details on the company’s Revenue and valuation.

[Updated 11/12/2020] Snowflake Stock: 3 Key Risks

Snowflake (NYSE: SNOW), the cloud-based data warehousing company that went public in September, is valued at over $65 billion, or about $240 per share. Below, we take a look at some of the key risks that the company faces.

Snowflake’s software enables organizations to manage and analyze large quantities and diverse types of data across public clouds such as Amazon’s

AMZN

GOOG

MSFT

Snowflake stock also has considerable valuation risk, considering that it trades at about 115x projected FY’21 revenues, compared to the broader software space that trades at about 8x Revenues. [1] At these valuations, the company has very little room for error and needs to execute to perfection to justify its stock price. Moreover, Snowflake’s public float – which is the number of shares held by public investors – is quite low, with the company offering just 28 million shares or about 10% of its total shares outstanding during its IPO. The low supply of shares is no doubt a major reason the stock has rallied so much since its listing. With Snowflake stock up about 2x from its IPO price, it is very likely that employees and investors could cash out when the post IPO lockup period expires in March 2021, putting downward pressure on the stock.

[Updated 10/21/2020] Snowflake Vs. Palantir

The last month saw Palantir (NYSE: PLTR) and Snowflake (NYSE: SNOW) – two relatively high profile software players go public. Snowflake’s software enables organizations to manage and analyze large quantities and diverse types of data across public clouds such as Amazon’s AWS in a single, easy to use platform. Palantir offers big data and analytics solutions primarily used by governments and intelligence agencies, although it has been expanding its presence in the commercial space.

While the two companies are focused on big data, investors are valuing them very differently. Snowflake stock trades at over 120x projected FY’21 Revenues (FY ends January) while Palantir trades at just about 15x projected FY’20 Revenues (FY end December). Does this make sense? How do the companies compare in terms of business models, revenue growth rates, and margins? We provide more details below.

See our interactive analysis on Snowflake’s Valuation and Palantir’s Valuation for more details on the two companies’ valuation.

Revenues & Growth Rates

Palantir’s Revenues grew by 24% to about $740 million in 2019 and growth is likely to pick-up to levels of over 40% in 2020 as Covid-19 related disruptions increased demand for the company’s services. In comparison, Snowflake saw Revenue grow 173% from $97 million in FY’19 to about $265 million in FY’20, although the growth rate is likely to slow down to roughly 110% over the current fiscal based on consensus figures. Overall, Snowflake’s Revenues should grow at a higher rate compared to Palantir, considering its SaaS-based model which can scale to a large base of customers with much less customization. Palantir, on the other hand, needs engineers to adapt its tools to the unique needs of customers. Snowflake had over 3,100 customers as of July 2020, compared to Palantir which had about 125 customers as of its last fiscal year.

Profitability

While Palantir is slightly ahead in terms of profit margins considering that it is the more mature company (Palantir was founded in 2003 versus Snowflake which was founded in 2012), we expect Snowflake to be more profitable in the long-run given its relatively more standardized product and lower customer acquisition costs. Snowflake posted a Gross Profit Margin of 62% for the first six months of FY’21, with Operating Margins standing at -72%. Palantir’s Gross Margins stood at about 72% over the first six months of 2020, with Operating Margins coming in at about -35%.

Valuation

Snowflake stock has more than doubled from its IPO price of $120 to about $250 currently, valuing the company at about $70 billion. Palantir, on the other hand, hasn’t moved too much since its listing and is valued at about $15 billion. There are a couple of reasons for Snowflake’s premium valuation. Firstly, the company is growing much faster than Palantir and should also be more profitable in the long-run given its highly scalable delivery model. Investors have also been paying a big premium for growth stocks. Secondly, unlike Palantir which has high exposure to government contracts – particularly in areas related to surveillance and national security – causing transparency and perception issues, Snowflake’s business is focused on more commercial customers.

That said, Snowflake has considerable valuation risk, considering that it trades at about 122x projected FY’21 revenues, compared to Palantir which trades at just about 15x projected 2020 Revenues. The story could change quickly. If Snowflake’s growth rates slow down, with the company facing competition from cloud majors such as Amazon and Google who offer their own data warehousing solutions, investors could re-think its valuation. On the other side, investors could double down on Palantir stock if they see more proof points indicating that the company is making progress in the commercial sector, via high profile deals or stronger Revenue growth.

[Updated 9/29/2020] Putting Snowflake’s Valuation Into Perspective

Snowflake (NYSE: SNOW), the cloud-based data warehousing company that went public recently, is valued at about $60 billion, or about $220 per share. The company trades at a whopping 230x trailing Revenues – well above many other high-growth SaaS names. Can Snowflake justify this valuation? In our interactive dashboard analysis on Snowflake’s Valuation: Expensive Or Cheap we break down the company’s revenues and valuation and compare it with other high-growth software players. Parts of the analysis are summarized below.

A Brief Look At Snowflake’s Business & Risks

Snowflake’s software enables organizations to manage and analyze large quantities and diverse types of data across public clouds such as Amazon’s AWS, Google Cloud, and Microsoft’s Azure in a single, easy to use platform. Snowflake stands to benefit as businesses increasingly move to the cloud while leveraging big data and artificial intelligence. Although major public cloud players have their own data warehousing solutions, (Amazon’s AWS offers Redshift, while Google offers BigQuery), Snowflake’s platform offers more flexibility compared to rivals and works well across platforms. However, the big cloud players have a strong incentive to promote their own warehousing offerings, as it enables them to lock customers into their platforms and services. There is a possibility that these companies could use their vast resources and control over their respective platforms to gain an edge over Snowflake.

Snowflake’s Revenue

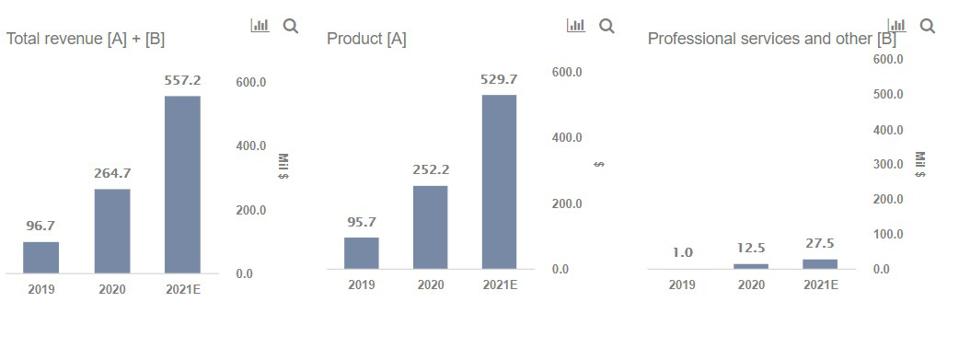

Let’s take a closer look at what’s driving Snowflake’s Revenue. Snowflake has two operating segments. 1) Products, which include Snowflake’s core data warehousing solutions. Customers pay according to the compute and storage that they use. 2) Professional Services – which includes consulting, on-site technical solution services, and training related to the platform.

Snowflake’s Product Revenue grew from $96 million in FY’19 to about $252 million in FY’20, as the company grew its customer base by 152% from 948 in FY’19 to 2,392 users. Based on the historical growth rate, and growth over Q2 (it had 3,117 customers as of July 2020), we expect Snowflake’s customer base to grow to about 4,600 in FY’21, with total Product revenues coming in at about $530 million. Snowflake’s Total Revenue, which includes its revenue from Professional Services grew from $97 million in FY’19 to about $265 in FY’20 and we expect it to grow 110% to about $557 million in FY’21.

Now Snowflake is not only adding new customers at a rapid clip, but it is also better monetizing its existing users. Snowflake’s Net Revenue Retention rate – which is the percent of revenue retained from the prior year after factoring for upgrades, downgrades, and churn – stood at 158%, indicating that existing customers continue to spend more.

Trefis

Why Is Snowflake’s Trading At Such A Premium?

With benchmark interest rates at near-zero levels, investors have generally been paying a premium for growth. However, Snowflake stock, which trades at about 110x our projected FY’21 revenues for the company and over 230x FY’20 revenues appears pricey. Let’s compare Snowflake with other high growth SaaS and database players. Datadog trades at 76x trailing revenues and posted 83% revenue growth in 2020. Okta trades at 25x trailing revenues and posted 46% growth over its most recent fiscal year. MongoDB trades at 22x and posted 58% growth.

Sure Snowflake is growing faster than these companies, but there is another reason why the stock could be trading so high, namely a low supply of shares. Snowflake’s public float – which is the number of shares held by public investors – stood at just 28 million shares or about 10% of its total shares outstanding, and the low supply of shares is likely to have caused a bid up in the price. With Snowflake stock up almost 2x from its IPO price, it is very likely that employees and investors will choose to cash out as the post IPO lockup periods expire, putting downward pressure on the stock.

Trefis

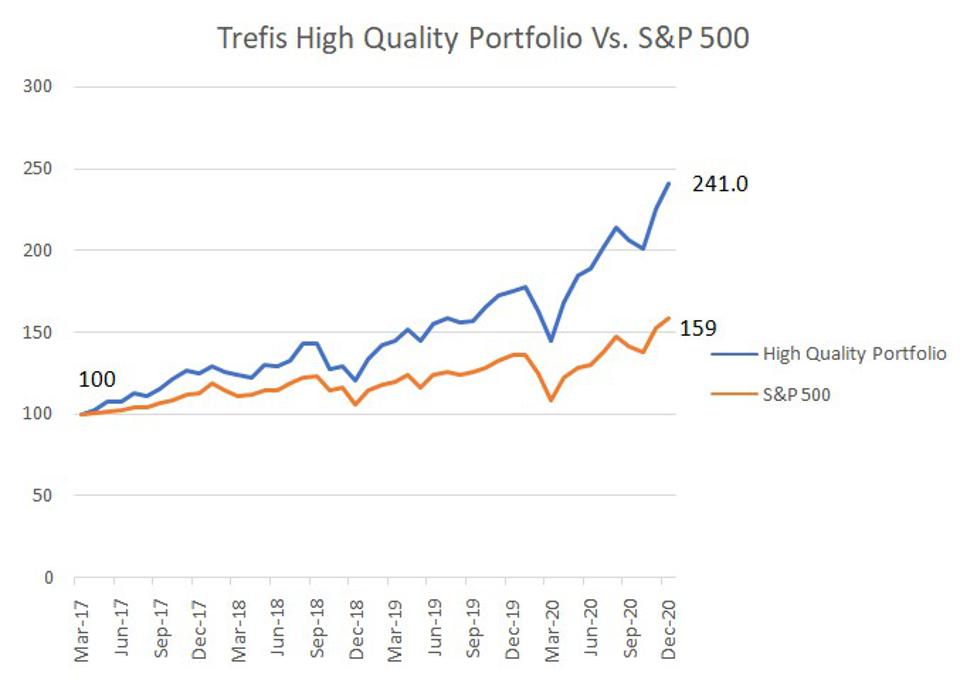

While Snowflake offers high growth, we think it comes with considerable risk at current prices. What if you’re looking for a more balanced portfolio instead? Here’s a high-quality portfolio to beat the market, with over 100% return since 2016, versus about 55% for the S&P 500. Comprising companies with strong revenue growth, healthy profits, lots of cash, and low risk, it has outperformed the broader market year after year, consistently.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Recent Comments