{kind=link}

As rough as it was in managing the supply chain roiled by the Coronavirus pandemic in 2020, this year calls for even greater agility and creative collaboration, according to the annual State of Logistics (SOL) report.

“Logisticians came off the ropes of a bruising 2020 with a new appreciation that, while resilience resulting from the capabilities they had built got them through the main disruptive rounds of the pandemic, 2021 is confirming that the ability to change plans and execute under adversity has risen to be the top priority,” said Michael Zimmerman, partner with the Kearney consulting firm and the report’s lead researcher.

Kearney consultants put together the 2021 report, titled “Change of Plans,” which is sponsored by third-party logistics provider Penske Logistics on behalf of the membership of the Council of Supply Chain Management Professionals (CSCMP). The annual SOL report has been produced in various forms over the past 32 years.

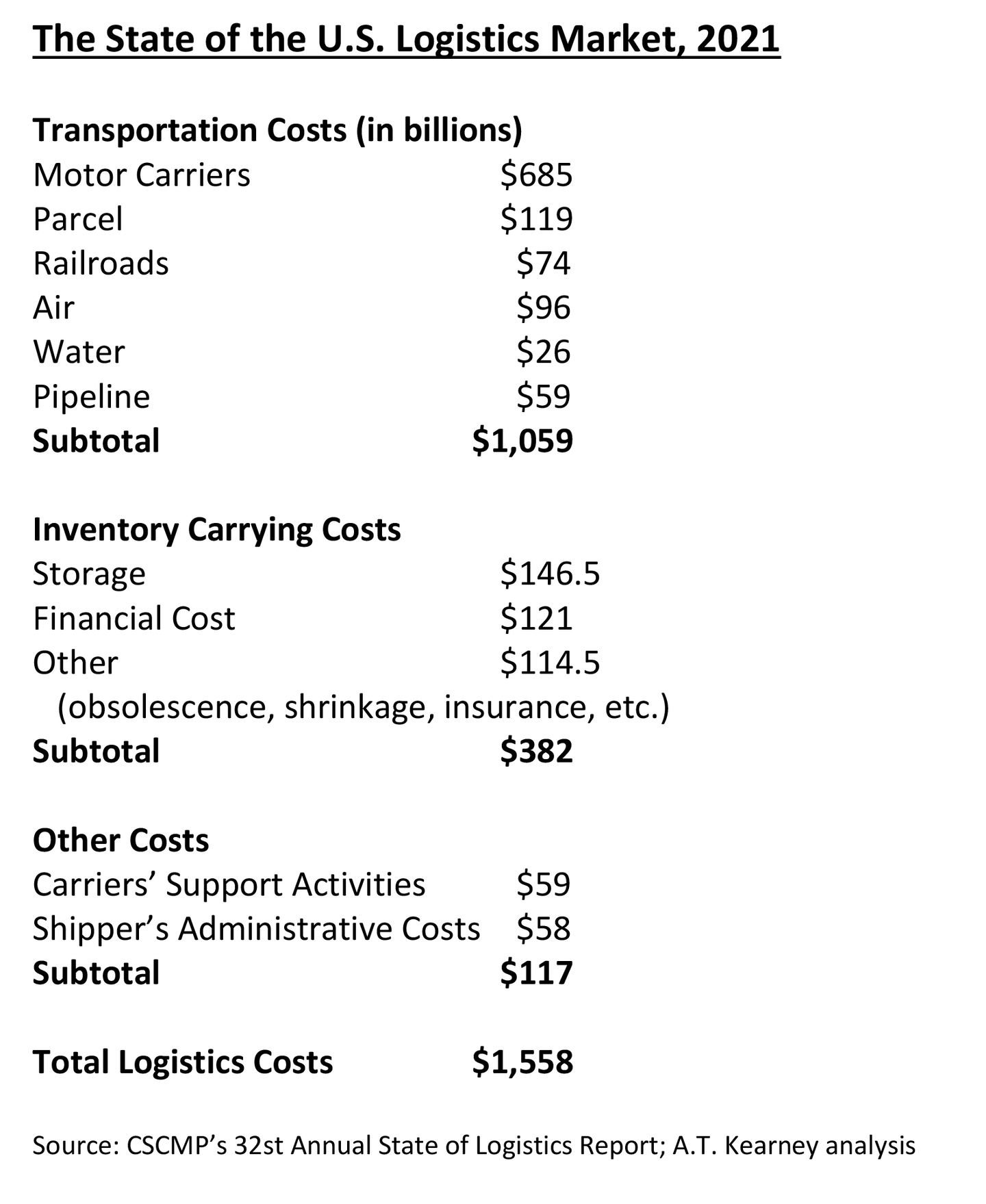

In 2020, United States business logistics costs (USBLC) fell 4.0% to $1.56 trillion, representing 7.4% of the year’s $20.94 trillion GDP. The pandemic made shippers’ and carriers’ assets less efficient and destroyed any idea of predictability, the researchers concluded. “While service outcomes largely deteriorated, logistics was remarkably effective given the disruptions.”

The U.S. economy is now expected to grow by 7.7% in 2021, and the global economy by 6.3%, barring unforeseen developments. In fact, such disruptions are sure to continue. “The pandemic’s aftereffects and new surprises will force continuous plan redevelopment and adaptation,” the researchers wrote.

In 2020 transportation costs rose by 0.8%. This was far less than the 4.7% growth in 2019, or the 10.4% rise in 2018, but certainly a contrast to an economy that shrank overall. The increase was driven by a 24.3% expansion in the parcel and last-mile segment, as e-commerce and home delivery exploded.

Looking at the other transportation modes can be deceptive because of unique situations that arose during the pandemic, such as congestion at ports and the disruption of over-the-road trucking by lockdown measures and other factors.

Warehousing growth remained strong in 2020, the researchers noted. Many industry fundamentals were up from a record-setting 2019. Net absorption increased 11%, to 268 million square feet. Asking rents grew at a faster rate than the previous year, to $6.76 per square foot. While the vacancy rate was higher than last year, it was still remarkably low.

In short, e-commerce spurred continued high demand for warehousing space. The pandemic shifted many consumers to online shopping, which boosted needs for warehouse space. Providers, especially of urban last-mile facilities, hurried to keep pace. This effect then outlasted the spring 2020 restrictions placed on physical retail stores.

Managing Warehousing’s Boom

Fourth quarter 2020 warehouse leasing volumes were 26.9% higher than 2019. Vaccine distribution added further pressures in early 2021, especially for cold storage. But even as vaccine pressure fades, other demands will keep capacity tight, the researchers believe.

“E-commerce fulfillment centers are a special category of warehouse, ideally featuring high ceilings and multiple mezzanine floors,” the report contends. “There’s demand for very large facilities (3+ million square feet) and for downtown urban facilities.” Also in demand by customers are advancements in technology and sustainability.

With rising e-commerce and a new appreciation of the dangers of supply chain disruptions, businesses will likely increase safety stock drastically, which will require a greater warehouse footprint, the researchers explained. “Greater inventory requires both more space and more management oversight.”

The warehousing labor market has been tight for years, and COVID-19 didn’t change its basic characteristics, including seasonality and difficult working conditions. Beyond competitive compensation, warehouses could attract workers by emphasizing safety and flexibility, factors that the pandemic brought to the fore, the researchers suggest.

“Warehouses vary in supplying personal protective equipment (PPE) materials, enforcing enhanced protective measures, and offering flexible scheduling,” they said. “Enhanced training programs and standard retention strategies (tracking key performance indicators for retention, conducting robust exit surveys, and so on) can also help improve conditions for workers.”

Kevin Smith, the report panel presentation chair and president of Sustainable Supply Chain Consulting, observed, “Inventory ratios are now virtually one-to-one. They have never been that low before. That means that companies have about one month of inventory. Years ago, that would have been a problem because of lack of visibility to manage them properly. This is going to be a big challenge, but it is a challenge that the supply chain is up to.”

He added, “I don’t think we should stay at one-to-one over the long term because it would hurt our ability to service customers and hurt the ability to give consumers what they want. Right now, we seem to be doing good, but one-to-one is a scary number.”

Of course, the labor shortage also is accelerating adoption of automation and other technology in warehouse and distribution operations. The warehouse automation market is projected to grow at a CAGR of 14% to reach $30 billion by 2026. “The pandemic may serve as a tipping point for warehouse automation,” the researchers pointed out. “Fast-moving inventory requires more touches, and using robots helps minimize employee interaction that spreads the virus.”

Operating during a period of increased operational complexity, robots reduce losses related to employee turnover, they note. At large warehouses, shuttle systems and massive data analysis can improve productivity and the ability to flex labor. At smaller warehouses, improved technology is reducing the payback period for automated guided vehicles (AGVs) and autonomous mobile robots (AMRs).

The vast majority of American warehouse companies also offer a large range of third-party logistics (3PL) services. The researchers note that 3PL services—both asset-based and non-asset-based—were in great demand last year and that will continue to be the case in the future. The continuing disruption experienced by the economy also creates opportunities for 3PL providers of all stripes. In turbulent times, the deep knowledge and wide network of a 3PL become more valuable.

Yet turbulent times place increasing pressure on the 3PLs to have developed the right strategies in the past and to implement the right insights in the present. In 2020—and moving forward through 2021—those 3PLs that prioritized resilience will become the dominant leaders in the segment, the report predicts.

Jack Be Nimble, Jack Be Quick

“This year the story is one of adaptation under the most severe conditions in memory. Shippers and carriers had to continuously change plans as the means of logistics they relied on strained and sometimes broke,” stressed research leader Zimmerman during the report’s presentation and panel discussion held virtually on June 23.

“Moving forward, supply chains must continue to provide goods and services to the American public while dealing with tight capacity and volatile rising [carrier] rates. The first half of 2021 has the highest rates the market has ever seen,” he added.

Zimmerman’s fellow panel members, who were drawn from different corners of the logistics industry, agreed with and amplified many of his views.

Matthew Hill, head of the North American import market for Maersk, the Danish ocean and inland shipping company, also said the COVID-19 changes to the economy forced supply chain managers to adapt to rate change. “When you look at what worked and what didn’t work in the past year, it’s been all about which customers were the most nimble, who were willing to try something a little bit new and different, outside of the box or that they weren’t used to, even if it cost a little bit more.”

He added, “When you have that ability, then we can go to our rail and trucking partners and lock up something that will provide some sort of guarantee in the supply chain that otherwise potentially wouldn’t exist during a difficult time.”

Hill believes this will continue to be important as time progresses. “Being nimble and flexible is super-important. You need to collaborate with your providers and your partners to continue to co-develop and co-create alternate solutions because that is the path forward now, the new normal.”

Andy Moses, senior vice president of sales and solutions for Penske Logistics, declared that he agreed 100% with Hill. “Collaboration, listening and probing are very important right now, specifically if you want to really understand what carriers are working with—equipment shortages and things like that. Clearly, it is a good time to find ways for eliminating waste between the parties to make the system as efficient as possible,” he explained.

“Resiliency, innovation, technology, and close collaboration with shippers have all been essential to weathering the rapidly changing market demands up and down the supply chain,” Moses added. “We see this continuing as supply chains reset and adjust to a new normal as consumer preferences and expectations reshaped the future of the supply chain during the pandemic.”

However, Alan H. Shaw, executive vice president and chief marketing officer for Norfolk Southern Railroad, believes the changes we experienced last year were actually nothing all that new for many experienced logisticians. “We’ve all been really good about optimizing our networks in the past. What we haven’t done a very good job of is optimizing the touchpoints in between the different components of the supply chain eco-system. The companies that learn how to do that best are going to be the ones that win because they will have the solution that clears the market.”

The other panel members also emphasized that network optimization will be the key to success in the future. “Optimizing networks is particularly important,” Marc Althen, president of Penske Logistics, stressed. “Networks are not static, so taking a look at the optimal number and location of facilities in the supply chain network is a simple best practice, even if it takes some doing to do it right, but there is a lot of carbon reduction that can come out of it. We are busy with a lot of customers doing that kind of work these days.”

Moss argued that the key to success in this area is the emergence of control tower technology, which helps manage the various silos in the supply chain that are organized around data and around visibility. “This is an area of development that I think offers broad promise.”

The researchers agreed and added a new chapter to this year’s report on this kind of technology. “In a world of increasingly abundant information, the control tower serves as an information hub to enable better decisions,” they said.

IBM defines a supply chain control tower as a connected, personalized dashboard of data, key business metrics and events across the supply chain. A supply chain control tower enables organizations to more fully understand, prioritize and resolve critical issues in real time.

From a data perspective, control towers offer the necessary visibility by connecting systems across every aspect of the supply chain, the report explained. “Although end-to-end visibility is a daunting feat, for most shippers, pooling the data is only half the battle. Implementing solutions to enact resilience requires expertise, resources, and a network fortified with assets—barriers that seem insurmountable to the average shipper and carrier.”

This presents a unique opportunity for 3PLs, according to the researchers. “For most shippers, the biggest barriers to building and offering control tower capabilities are in building an expansive network,” they said. “Because 3PLs have already overcome those barriers, they are best positioned to implement successful control towers. As the world moves toward data-driven decisions, this will become a key strategy for 3PLs.”

Is the Last Mile Sustainable?

Managing the last mile of e-commerce transactions is a particularly thorny issue for logisticians and is likely to remain one in the future. One challenge involves labor, Moss pointed out, because other economic players are competing for the labor that normally would be working in warehouses and other final-mile delivery operations. “There is quite a bit of stress behind the scenes with carriers trying to navigate and keep up with the fast growth in this segment,” he said.

The nature of last-mile delivery as it is presently operated is literally not sustainable—at a time when companies are scouring their supply chains for places where they can eliminate waste and reduce their carbon footprint, Smith believes.

“E-commerce and sustainability are not compatible,” he said. “The inefficiencies driven by last-mile delivery really hurt sustainability more than they help it. We are going to have to balance those two in the future.” (However, others have disagreed with this view.)

A week after the SOL report presentation, Amazon announced that its carbon footprint grew 19% in 2020, including an 18% rise in emissions from fossil fuels. The calculations included emissions totals for the Amazon Whole Foods subsidiary. This followed the company’s report of a carbon emissions footprint increase of 15% in 2019. In June, Amazon also announced that it leased 12 additional Boeing 767s for its fleet, now said to total more than 80 aircraft.

One solution that may lie ahead involves segmenting consumers in terms of differing delivery needs, Zimmerman contended. E-commerce companies already have been looking at which customers really require high levels of service, which ones are willing to wait a few days for a delivery, and how that varies.

“This is very much top of mind for shippers,” he said. “They are working with their marketing people and consumer surveys to see how they can segment this service. In the meantime, the carriers and providers are trying to get better at ‘densifying’ the delivery network to lower the cost of a delivered package because there is no sign that this growth of e-commerce and last-mile is abating.”

When it comes to sustainability, Smith said that in spite of all the other pressures that have exerted themselves on the supply chain over the past year, 3PL providers have noticed that their clients have remained steadfastly committed to sustainability throughout. He cited a yet-to-be released CSCMP study where 83% of survey respondents said they are actually in the process of accelerating their sustainability efforts.

“I think this is an effort by large companies to chase down and drive efficiencies into the business, he added. “There is a tremendous impetus for 3PLs to work with customers who want to be focused on sustainability. It’s an active topic with most customers. Sustainability is corporate responsibility, and sustainability also is old-fashioned good business for both parties.”

Smith cited the continuing interest in electric vehicles, eco-facilities, and practices involving improved routing, load utilization and internal container management. “There are so many areas where we work together on sustainability that it is no surprise that it is top of mind today.”

Norfolk Southern’s Shaw added, “The pandemic accelerated a lot of trends that were already there. There will be more positioning of inventory closer to the ultimate consumer. There will be more risk-aversion inventory stockouts than there were before and a greater focus on capacity.”

He also has noticed that the railroad’s customer expectations are now driven by their personal experiences in the consumer world. This includes expectations of greater transparency and visibility, sustainability, and onshoring, off-shoring and rightshoring. “I think it will be very exciting for us because we all will have better tools with which to do all that.”

Recent Comments